The IRA is a retirement account for individuals that offers an accessible retirement savings vehicle for all investors. Money can be contributed directly or rolled over from an employer retirement account like a 401(k). There are two types of IRAs, here is a look at both the traditional and Roth IRA to help you decide which is right for you.

For both 2021 and 2022 the contribution limits for both types of IRAs combined is $6,000 with an extra $1,000 catch-up contribution for those who are 50 or over. Contributions for the 2021 tax year can still be made through April 15, 2022.

Roth IRA Overview

Roth IRA contributions are made on an after-tax basis. The money in the account grows tax-free and can be withdrawn tax-free if certain conditions are met. These include being at least age 59 ½ and having met the applicable five-year rule for the account pertaining to contributions and/or conversions and rollovers into the account. If you are younger than 59 ½ and don’t meet certain requirements, then your withdrawal could be subject to taxes and/or a 10% penalty.

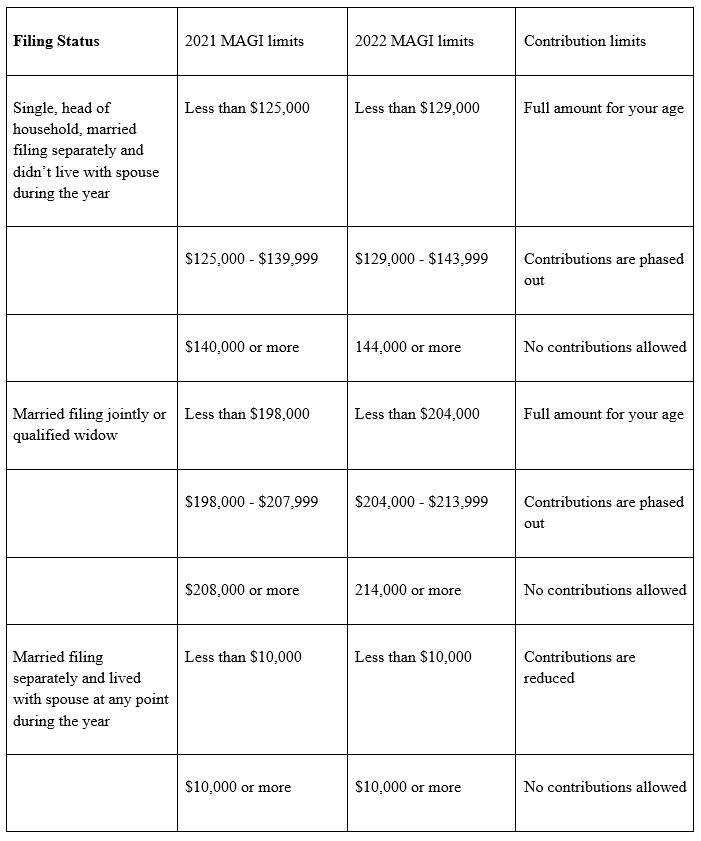

There are income restrictions on your ability to contribute to a Roth IRA. They are based on your MAGI (modified adjusted gross income). For 2021 and 2022, the limits are:

There are a number of pros and cons to a Roth IRA.

Some of the Pros include:

- Withdrawals are tax-free in retirement if certain requirements are met.

- Your contributions to the account can always be withdrawn tax-free.

- There are no required minimum distributions (RMDs) for a Roth IRA.

Some of the cons include:

- There is no tax break for contributions in the year they are made.

- If your income is too high you cannot contribute to a Roth IRA.

A Roth IRA is best for someone who:

- Is likely to be in a high tax bracket in retirement.

- Who wants to avoid the impact of RMDs.

- Who wants to be able to pass IRA assets to non-spousal beneficiaries tax-free.

Traditional IRA Overview

Traditional IRA contributions can be made on a pre-tax basis. If you are covered by a retirement plan at work, such as a 401(k), then there are income limitations on the amount that can be contributed pre-tax. If your pre-tax contributions are limited or prohibited, you can make after-tax contributions to the account up to the $6,000/$7,000 limits.

Withdrawals from a traditional IRA are taxed as ordinary income with the exception of the value of any after-tax contributions. Withdrawals prior to age 59 ½ may be subject to a 10% penalty, with some exceptions.

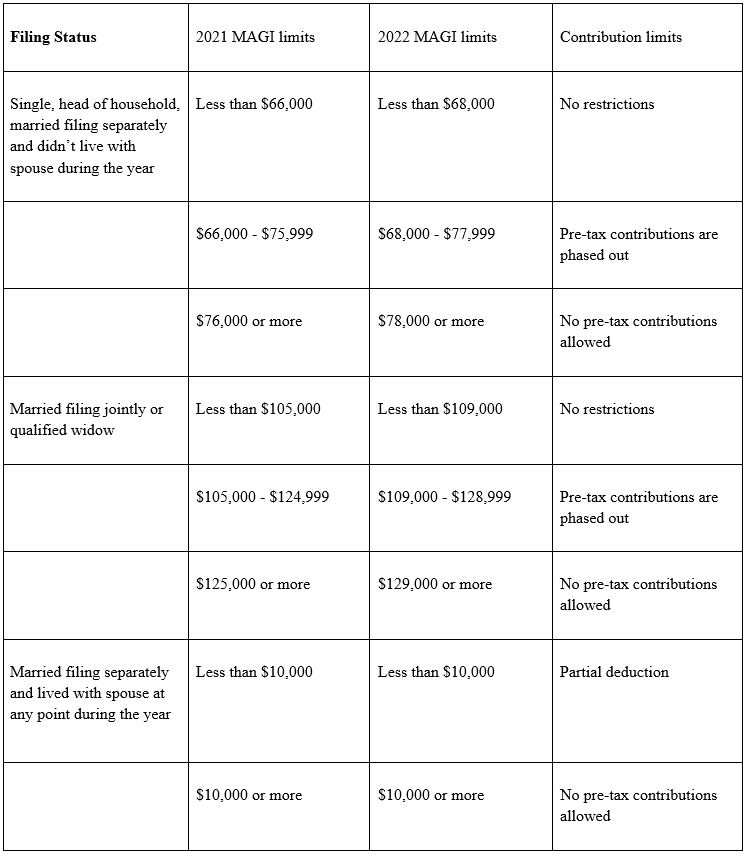

There are income restrictions on your ability to contribute on a pre-tax basis to a traditional IRA if you are covered by a workplace retirement plan. They are based on your MAGI (modified adjusted gross income). For 2021 and 2022, the limits are:

Note there are additional restrictions in situations where you are not covered by a plan at work, but your spouse is if you are married.

There are a number of pros and cons to a traditional IRA:

Some of the Pros include:

- Pre-tax contributions are available if you meet the income requirements.

- Your investments grow on a tax-deferred basis.

Some of the cons include:

- Distributions from the account are taxable.

- Traditional IRAs are subject to required minimum distributions.

- Your ability to make pre-tax contributions may be limited if you are covered by a retirement plan at work if you earn too much.

A traditional IRA is best for someone who:

- Is likely to be in a lower tax bracket in retirement.

- Who wants to take advantage of the ability to make pre-tax contributions if eligible.

James Bailey of Bailey & Quinn Financial Consulting Group says, “As a rule of thumb for those considering a Roth or traditional IRA, the anticipated tax bracket at retirement is key. If you think you’ll be in a higher bracket when you retire, a Roth IRA may be the better choice.”

Contact your Wedbush advisor to discuss which type of IRA is best for you and how to best manage an existing IRA account.

Looking to build a financial plan based on your goals while considering market trends and risk factors? Click here to check out our approach to Wealth Management.

Disclosure

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information presented is not intended to constitute an investment recommendation for, or advice to, any specific person. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. The information in these materials may change at any time and without notice.